Accounting Before Coin: Mesopotamia’s Ledger Money (c. 3300–2000 BCE)

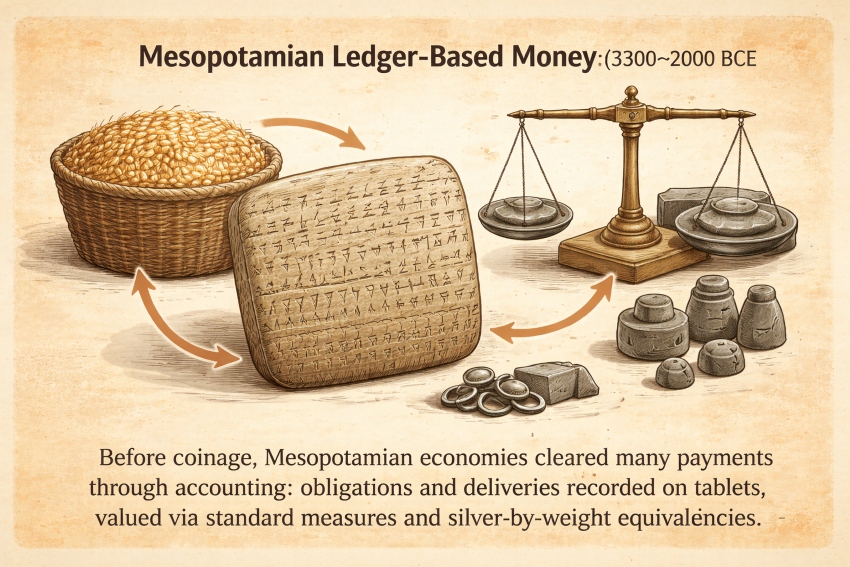

“Illustration of Mesopotamian ledger-based money: a cuneiform tablet, balance weights, barley rations, and silver by weight.”

Summary of events during the period

The earliest “money” systems we can document in detail are not coin-based. In early Mesopotamia, large institutions (temples and palaces) ran economies through accounting, standardized measures, and credit, using clay tablets as durable records of obligations, deliveries, and rations. This created a practical payment system: values were computed in stable units of account (not necessarily paid out as physical objects in every transaction).

Payment media (what people used to pay)

- Grain rations (especially barley) distributed to workers and dependents as standardized monthly allocations. A surviving example is a British Museum tablet recording barley rations for a large workforce, showing how provisioning and “payment” could be administered at scale.

- Silver by weight (not coined): used as a high-trust reference value and frequently as a unit of account. In the Ur III period, accounting texts commonly value goods through silver-based equivalencies; one documented normative relationship is 1 shekel of silver = 300 sila of barley in parts of the administrative system.

- Seals and standard weights/measures: not “money” themselves, but crucial payment infrastructure—enabling verification, auditing, and enforcement in a world where settlement often meant “updating the ledger.”

How prices were set (negotiated vs administered vs regulated)

Mixed regime:

Administered equivalencies (institution-led)

- Much of what survives is institutional accounting. Prices often appear as recorded ratios (e.g., barley:silver), consistent with an administrative need to convert varied goods into a common value metric for rationing, taxation, redistribution, and auditing.

Negotiated variation (market activity within and around the system)

- Some merchant and commodity accounts show non-uniform ratios (e.g., wool:silver or barley:silver ratios that vary across texts), which is difficult to explain if every price were purely fixed by decree. A defensible interpretation is that institutional norms existed. But real transactions could deviate based on conditions, quality, locality, timing, and bargaining power.

What we can say confidently

- The record supports “prices” as operational facts, used for conversion and settlement. While the evidence base is biased toward large-institution bookkeeping rather than everyday haggling in small markets.

How payments cleared (the “rails”)

- Clearing by account: Many payments effectively cleared when an institution (or a household with scribal capability) recorded that an obligation was created, transferred, or discharged—analogous to a modern ledger entry. Proto-cuneiform and early cuneiform corpora are fundamentally bookkeeping technologies designed to preserve such quantitative claims.

- Settlement in goods and/or silver-by-weight: Depending on the context, settlement could mean delivering barley, labor, textiles, livestock, or silver—while the ledger maintained comparability across these categories through standardized metrology and equivalencies.

Trust and governance (why anyone accepted it)

- Institutional authority: Temples/palaces enforced claims and organized production/distribution. Tablets served as durable audit trails.

- Standards: Trust was also technical—weights, measures, and scribal conventions made value legible and transferable across time and parties.

Revenue model (who made money from the system)

- Interest-bearing credit: Loan documents show standardized interest conventions in later 3rd-millennium practice, including commonly cited rates such as 20% on silver and 33% on barley in Ur III material (with important variation by context).

- Institutional surplus extraction: Beyond explicit interest, large institutions captured surplus through rents, obligations, and controlled redistribution—“revenue” expressed as flows of goods, labour, and claims recorded in the accounting system.

Failure modes and constraints

- Agricultural volatility: Barley-based obligations are exposed to harvest shocks; when repayment depends on next season’s output, bad harvests can destabilize household balance sheets.

- Documentation bias: Our clearest lens is institutional; everyday market negotiation is harder to reconstruct, so strong claims should be anchored in the administrative and legal record that survives.

What scaled it (the scaling technology)

- Writing as infrastructure: Early writing systems in Mesopotamia are deeply tied to accounting needs—standardizing and transmitting quantitative information across administrators, time, and distance.

- Metrology + standard conversions: Shared units (e.g., shekel, sila) and recorded equivalencies made multi-commodity economies computable and governable.

Caption

“Before coinage, Mesopotamian economies cleared many payments through accounting: obligations and deliveries recorded on tablets, valued via standard measures and silver-by-weight equivalencies.”

Sources

- Robert K. Englund, Proto-Cuneiform Account-Books and Journals (CDLI PDF). CDLI

- Oxford Academic (chapter), Accounting in Proto-Cuneiform (overview of archaic accounting methods). OUP Academic

- E.L. Cripps, The Structure of Prices in the Neo-Sumerian Economy (I) (Ur III; silver/barley equivalencies). CDLI+1

- E.L. Cripps, Barley:Silver Price Ratios (compiled attestations; Ur III price ratio evidence). CDLI

- British Museum collection object: clay tablet recording barley ration distributions (example of administered payments). British Museum

- Steven J. Garfinkle, Some Observations on Lending Practices in Ur III (interest conventions; loan practice). Simon Fraser University

- E.L. Cripps, The Wool:Silver Price Ratio (evidence of ratio variation; not purely fixed pricing). CDLI