Islamic and Indian Ocean Commercial Finance: Trust, Contracts, and Long-Distance Settlement (c. 700–1200)

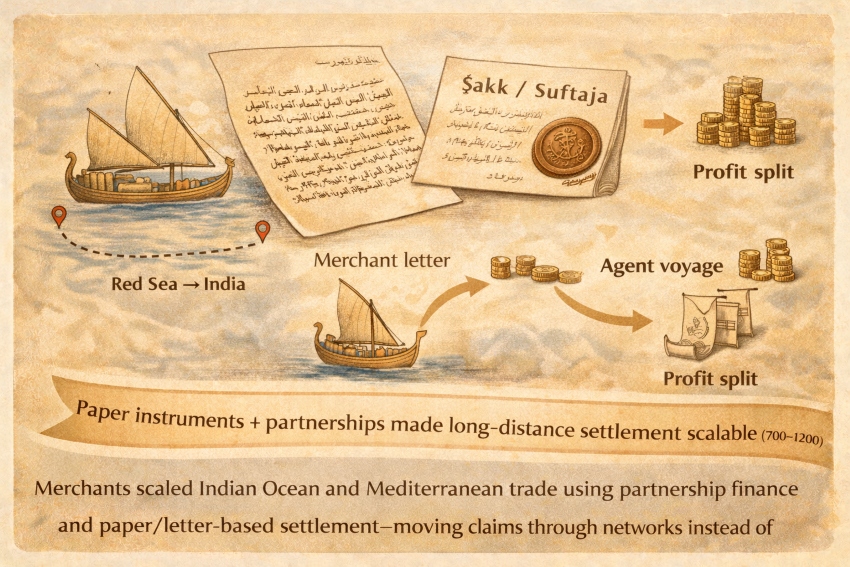

“Merchants scaled Indian Ocean and Mediterranean trade using partnership finance and paper/letter-based settlement—moving claims through networks instead of moving coin.”

Summary of events during the period

From roughly 700 to 1200, long-distance commerce across the Islamic world and the Indian Ocean expanded using a toolkit of legal contracts, partnership finance, and paper/letter-based payment instruments that reduced the need to move coin physically. The historical record is unusually rich for the 11th–13th centuries due to documentary corpora such as the Cairo Geniza, which preserves merchant letters, accounts, and legal deeds describing real-time trading operations between the Mediterranean, Red Sea, and Indian Ocean.

Payment media (what people used to pay)

- Coin (gold/silver/copper) remained foundational, but merchants increasingly aimed to avoid transporting large sums because it was risky and expensive.

- Partnership capital (qirāḍ / muḍāraba-type arrangements): an investor provides capital and an agent-trader conducts the venture; profits are shared by agreement, while losses (in principle) fall on capital, unless misconduct occurs. This structure is widely discussed as a core medieval Islamic commercial instrument and is often compared to the later European commenda.

- Money drafts / written payment orders (ṣakk): Encyclopaedia Iranica documents Arabic ṣakk used after the conquest as a money draft, including usage as a verb meaning to “write a money draft,” and notes later terms (e.g., softaja) increasingly used for related purposes.

- Bills for transferring funds over distance (suftaja): legal and historical literature treats the suftaja as a financial conveyance/transfer instrument discussed and debated by jurists, with particular attention to its permissibility and structure.

How prices were set (negotiated vs administered vs regulated)

Negotiated pricing (merchant practice)

- In the merchant world visible through letter collections and business accounts, prices are best modeled as negotiated: traders report market conditions, compare deals across ports, coordinate partners, and adjust buying/selling strategies in response to demand, risk, and shipping constraints. The Indian Ocean Geniza project explicitly highlights letters and accounts describing sourcing, buying, selling, shipping, and partnership coordination in “real time.”

Administered charges (state interfaces)

- Even where states did not “set” market prices, they shaped effective prices through customs, tolls, official brokerage rules, and port administration, which merchants explicitly plan around (including attempts to reduce or avoid charges, as noted in the Geniza project description).

Regulation through contract enforceability

- The most important “regulation” for pricing was often legal enforceability of obligations (partnership shares, repayment terms, and transfer instruments). The more predictable the enforcement environment, the more confidently merchants could price credit and risk.

How payments cleared (the “rails”)

- Debt transfer (hawāla / ḥawāla logic): scholarship on medieval Islamic payment methods describes hawāla as a transfer of debt/obligation, enabling settlement through reassignment rather than physical cash movement.

- Suftaja as remittance/transfer instrument: legal-historical treatments frame the suftaja as a tool for conveying funds/claims across distance, with juristic debate indicating that it was a recognized commercial practice requiring doctrinal evaluation.

- Money drafts (ṣakk): Iranica’s documentation of ṣakk as a “money draft” supports a clearing model in which written instruments represent and move claims—particularly valuable for inter-city trade networks.

- Partnership clearing via accounts and reporting: Geniza material (as summarized by modern research projects and overviews) repeatedly emphasizes partners operating in different localities, coordinating via letters and accounts—effectively a distributed settlement system where trust is maintained through documentation, reporting cadence, and reputational enforcement.

Trust and governance (why anyone accepted it)

- Commercial law + juristic scrutiny: The fact that instruments like the suftaja were debated by jurists is itself evidence of institutionalization: merchants used them enough to force legal clarification of what was acceptable.

- Reputation, correspondence, and verification: Documentary corpora show merchants managing trust through letters, accounting statements, and partner oversight, which substitute for centralized enforcement in far-flung routes.

- Stable contract forms: Udovitch’s work (and subsequent discussion) highlights how standardized partnership/commenda-like forms can reduce negotiation costs and clarify rights and obligations—key to scaling trade finance.

Revenue model (who made money from the system)

- Trade profit + risk pricing: Merchants earned margins on commodities (textiles, spices, metals) and priced shipping/credit risk into deal terms.

- Intermediation fees/spreads: Money changers, brokers, and agents earned through spreads, commissions, and informational advantage—especially where coin quality, weights, and multi-currency realities required expertise.

- Partnership profit shares: Qirāḍ/muḍāraba-type structures explicitly define profit allocation, enabling capital owners to earn returns without direct travel, while agents earn a negotiated share for execution.

Failure modes and constraints

- Counterparty risk across distance: Long-duration voyages and multi-agent chains create default and fraud risk; the system relies on documentation and reputation precisely because enforcement is costly at distance.

- Legal uncertainty and compliance constraints: Juristic debate over instruments (e.g., suftaja) shows that not all financial practices were uniformly accepted; legality could vary by interpretation and locale, constraining adoption or shaping design.

- Transport and political shocks: Maritime losses, piracy, war, and port disruption remain structural constraints on Indian Ocean commerce.

What scaled it (the scaling technology)

- Paper/letter instruments that move claims instead of coin: ṣakk/suftaja/hawāla-like mechanisms reduce transport risk and enable settlement through networks.

- Standard contract forms (partnership finance): qirāḍ/muḍāraba-type contracts allow capital pooling and agency scaling—an early “venture” logic suitable for long-distance commerce.

- Dense documentary culture (Geniza visibility): repeated reporting, accounting, and legal deeds turn trust into a managed system rather than a purely personal relationship—an essential ingredient for scaling networks.

Caption:

“Merchants scaled Indian Ocean and Mediterranean trade using partnership finance and paper/letter-based settlement—moving claims through networks instead of moving coin.”

Sources

- Princeton Geniza Lab — Indian Ocean Documents from the Cairo Geniza (letters, accounts, legal deeds; c. 1080–1240).

- Oxford Research Encyclopedia of Asian History — Jewish Merchants in the Indian Ocean Trade (Geniza-based visibility and networks).

- Geva, B. (2009) — The Medieval Hawale: The Legal Nature of the Suftaj… (hawāla debt transfer; suftaja legal framing).

- Lydon, G. (2019) — discussion of suftaja and juristic debate (OpenEdition PDF).

- Encyclopaedia Iranica — “ČAK” entry (Arabic ṣakk as “money draft”; term history and substitution by softaja).

- Udovitch, A.L. (1962) — At the Origins of the Western Commenda… (qirāḍ and commenda comparison; institutional significance).