Bretton Woods to Managed Floating: Dollar–Gold, Capital Controls, Eurodollars, and the Inflation Break (1945–1979)

“1945–1979 monetary order: Bretton Woods dollar–gold peg and par values, European clearing via EPU, SDR creation, Eurodollar offshore liquidity, 1971 gold-window closure, 1973 move to floating, and late-1970s anti-inflation pivot.”

Summary of events during the period

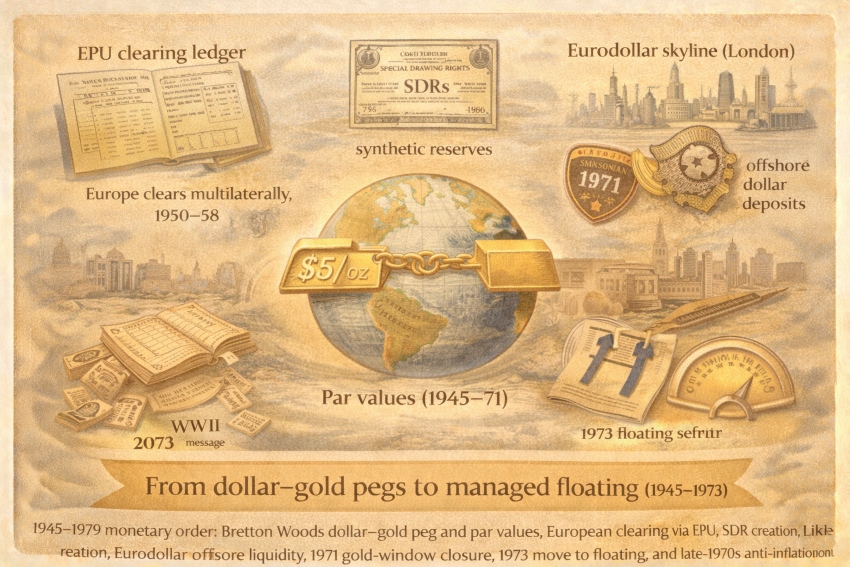

From 1945 to 1979, the global payments order moved through two distinct operating modes. First came the Bretton Woods par value system: “fixed but adjustable” exchange rates anchored to the US dollar, with the dollar linked to gold, and with extensive use of capital controls to preserve domestic policy space.

Second came the breakdown and replacement of that regime: escalating balance-of-payments tensions culminated in August 1971 (the “gold window” suspension), a short-lived attempt at repair (Smithsonian), a shift to generalized floating by 1973, and then the formal legalization of flexible exchange-rate arrangements through IMF reforms later in the decade (“Jamaica”).

The late 1970s added a final structural turning point: sustained inflation and energy shocks contributed to a credibility crisis that set the stage for the October 1979 Volcker policy shift toward breaking inflation expectations.

Payment media (what people used to pay)

- Bank deposits + cheques remained the domestic workhorses in advanced economies, with cash and notes for retail but bank money for scale.

- Dollar claims as the “global settlement language” during Bretton Woods: even when gold was the formal anchor, the practical reserve and invoicing reality increasingly relied on dollars and dollar assets. (This dynamic is central in Bretton Woods analyses and the later “par value” crisis narrative.)

- European Payments Union (EPU) clearing (1950–1958): a postwar mechanism to restore convertibility and enable multilateral settlement among European countries during reconstruction constraints.

- Offshore dollars (Eurodollars): by the late 1950s/1960s, banks in places like London accepted and created dollar deposits outside US jurisdiction, supplying global liquidity and bypassing some domestic constraints.

- IMF Special Drawing Rights (SDRs, created 1969): a supplementary reserve asset created when currencies were still tied to gold/dollar rules and global liquidity demand was rising.

How prices were set (negotiated vs administered vs regulated)

Negotiated prices (most goods and services)

- Most micro-level prices were still market-set. What changed was the macro price environment: exchange-rate rules and inflation dynamics increasingly shaped pricing behavior.

Administered anchor (the exchange-rate “price rule”)

- Under Bretton Woods, governments targeted declared par values (with adjustment permitted under defined conditions). The IMF Articles explicitly frame the system as one based on stable but adjustable par values when the par value system operates.

Regulated finance (financial repression and controls)

- Many countries relied on interest-rate management, bank regulation, and capital controls to defend parities and fund postwar states—reducing arbitrage but also pushing innovation into offshore markets (notably Eurodollars).

How payments cleared (the “rails”)

- IMF par value regime (1945–early 1970s): cross-border clearing aimed to preserve pegged rates through reserve management, policy adjustments, and (frequently) controls on capital movement.

- European multilateral clearing via EPU: instead of forcing immediate bilateral settlement after each transaction, EPU-style arrangements enabled multilateral positions and helped restore convertibility conditions in Europe by the late 1950s.

- 1971 break (Nixon shock): the US suspended the dollar’s convertibility into gold, effectively disabling the core Bretton Woods mechanism and triggering the final transition toward floating arrangements.

- Smithsonian “repair attempt” (Dec 1971): a coordinated realignment (including a new official gold price reference) that functioned as a temporary patch rather than a durable restoration.

- Generalized floating (by March 1973): the fixed dollar-based exchange-rate system was dropped and major currencies moved to floating.

- Messaging/operational infrastructure (SWIFT founded 1973): value still moved via banks and correspondent accounts, but instruction/confirmation increasingly relied on standardized secure messaging; SWIFT was created as a cooperative utility to replace telex-era friction.

Trust and governance (why anyone accepted it)

- Bretton Woods trust bargain: stability depended on confidence that the anchor currency and the gold link were sustainable, and that adjustment rules would be applied without triggering disorder. Scholarly reviews describe how an “adjustable peg” design evolved into something closer to de facto fixity in practice—raising the eventual cost of adjustment.

- Post-1973 governance through IMF surveillance + legal reform: the move to flexible arrangements required a new legitimacy framework; IMF histories of the 1970s reforms describe the contentious process of legalizing and structuring floating-rate reality.

- Credibility crisis of the 1970s: inflation and energy shocks undermined confidence in nominal anchors, setting up the political and technical conditions for regime change in monetary policy (culminating in 1979 in the US).

Revenue model (who made money from the system)

- Banks: earned on cross-border intermediation, FX spreads, trade finance, and (increasingly) offshore balance-sheet expansion (Eurodollar markets).

- States: benefited from the ability to run domestic macro policy with capital controls (at least for a time), while the anchor-currency country enjoyed substantial flexibility and financing capacity—one driver of the system’s internal tension as dollar liabilities grew faster than gold reserves could credibly back.

- International institutions: IMF/World Bank roles expanded from postwar reconstruction architecture to ongoing surveillance, liquidity instruments (SDRs), and crisis management as the regime changed.

Failure modes and constraints

- Reserve-drain and speculative pressure: fixed-rate systems become fragile when markets believe the peg is misaligned and reserves are insufficient—driving runs on reserves and forcing abrupt regime shifts (1971–73 is the canonical sequence).

- Control leakage and regulatory arbitrage: capital controls and domestic constraints pushed activity into offshore markets (Eurodollars), weakening the effectiveness of national boundaries in money creation and liquidity.

- Inflation entrenchment: the 1970s combined oil shocks with the loss of a stable international nominal reference framework, contributing to high and persistent inflation; this is explicitly emphasized in modern historical analyses of the decade.

What scaled it (the scaling technology)

- Institutional rails (IMF par values → surveillance frameworks): the key scaling move is not a gadget, but a governance stack that makes cross-border settlement predictable—first via par values, later via rules and surveillance suited to floating.

- Synthetic reserve assets (SDR): a direct attempt to supplement reserves and reduce over-dependence on a single national currency.

- Offshore balance-sheet money (Eurodollars): scaled global liquidity outside a single regulator’s perimeter.

- Standardized financial messaging (SWIFT): scaled operational reliability of cross-border payment instructions.

- Inflation credibility toolkit (1979 pivot): the Volcker shift is widely treated as a decisive credibility move to re-anchor expectations after the 1970s inflation experience.

Caption:

“Bretton Woods scaled stability via pegs and controls—then gave way to floating, offshore liquidity, and a new fight for inflation credibility.”

Sources

- IMF — Articles of Agreement (par value system; stable but adjustable par values). :contentReference[oaicite:29]{index=29}

- Bordo, M.D. (1993, NBER) “The Bretton Woods International Monetary System” (adjustable peg evolving toward de facto fixity; breakdown dynamics). :contentReference[oaicite:30]{index=30}

- Federal Reserve History — “Nixon Ends Convertibility of U.S. Dollars to Gold…” (Aug 1971). :contentReference[oaicite:31]{index=31}

- U.S. State Department (Office of the Historian) — “Nixon and the End of the Bretton Woods System, 1971–1973.” :contentReference[oaicite:32]{index=32}

- Federal Reserve History — “The Smithsonian Agreement” (Dec 1971 realignment). :contentReference[oaicite:33]{index=33}

- Riksbanken historical timeline — “1973: Bretton Woods goes to the grave” (shift to floating). :contentReference[oaicite:34]{index=34}

- IMF — “What is the SDR?” / SDR topic pages (created 1969; purpose as reserve asset). :contentReference[oaicite:35]{index=35}

- IMF eLibrary — “Agreement on Exchange Rates: Rambouillet and Jamaica” (legalizing floating via amendments). :contentReference[oaicite:36]{index=36}

- OECD / CVCE / IMF histories on EPU (1950–1958; multilateral clearing and convertibility restoration). :contentReference[oaicite:37]{index=37}

- Schenk (1998) “The Origins of the Eurodollar Market in London: 1955–1963” + BIS Quarterly Review (Eurodollar definition and regulatory drivers). :contentReference[oaicite:38]{index=38}

- SWIFT — “Our story” (cooperative founded 1973 to replace telex-era friction). :contentReference[oaicite:39]{index=39}

- Federal Reserve History — “Volcker’s Announcement of Anti-Inflation Measures” (Oct 1979 pivot). :contentReference[oaicite:40]{index=40}