Central Banking and the Credibility Problem: Paper, Convertibility, and Crisis Management (c. 1700–1840)

“Paper scaled payments, but stability required credibility: convertibility rules, crisis lending, and tighter note-issue governance.”

Summary of events during the period

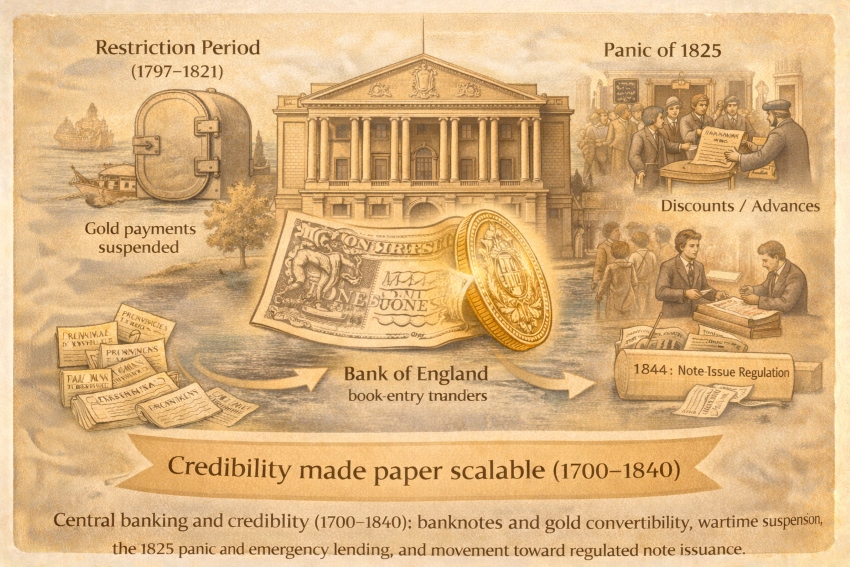

Between 1700 and 1840, “modern money” increasingly meant bank-issued liabilities (notes and deposits) supported—sometimes imperfectly—by convertibility into gold, and stabilized—sometimes reluctantly—by central-bank-like crisis lending. The period’s core tension was credibility: paper money scaled payments, but it also created the risk of runs, over-issuance, and systemic panics. Britain provides the clearest narrative arc: wartime suspension of convertibility (1797–1821), postwar restoration, recurrent crises (notably 1825), and then legislative moves to constrain note issue and improve stability—culminating just after this epoch in the 1844 Bank Charter Act.

Payment media (what people used to pay)

- Gold coin and gold convertibility as the anchor (when operating): Large-value confidence often depended on the expectation that credible notes could be exchanged for gold under established rules (or would return to that state after wartime disruption).

- Banknotes as mass-scale transaction media: Notes expanded practical liquidity beyond what coin supply could comfortably support—especially during war finance and rapid commercial growth.

- Provincial/country bank notes (a fragmented issuance layer): In Britain, numerous country banks issued notes, expanding local credit but also introducing uneven quality and heightened run risk—one reason Parliament debated tighter frameworks in the 1820s.

- Early European note experiments as context (Sweden): Although slightly earlier than this epoch’s start, Sweden’s experience shows the promise and danger of early paper: Stockholms Banco issued Europe’s first banknotes in 1661 and failed shortly after; Sweden later built a central banking tradition around the Riksbank.

How prices were set (negotiated vs administered vs regulated)

Negotiated prices (everyday market reality)

- Most prices were still set through bargaining and market conditions; what changed was the price level environment and the reliability of the monetary unit used in settlement, especially during suspension periods.

Administered conditions (convertibility rules as “price governance”)

- Convertibility policy effectively governs the “price of paper in gold.” When convertibility is suspended, the system shifts from a strict metallic constraint to a credibility regime: acceptance depends on whether people believe the issuer (and the state) will protect value and eventually restore the anchor.

Regulation via note-issue rules

- A key regulatory trend was to reduce instability caused by fragmented note issuance. Parliamentary debate in the 1820s explicitly worried about leaving currency issuance to many independent country banks with limited visibility into total circulation.

How payments cleared (the “rails”)

- Suspension as a payments regime (1797–1821): The Bank of England’s “Restriction Period” removed the obligation to exchange notes for gold, allowing paper to function as the primary settlement medium under extraordinary wartime conditions.

- Central-bank liquidity in crisis (1825 panic): Research based on detailed records shows that during the panic of 1825, the Bank of England reversed restrictive policy and lent aggressively—discounting bills and making advances—acting as a de facto stabilizer even before the “lender of last resort” doctrine was formally articulated.

- Branch expansion and note distribution (from 1826): The Bank of England began establishing provincial branches in 1826, expanding its note circulation and strengthening its presence beyond London—an infrastructure move tied to stability and distribution capacity.

- Toward constrained note issue (1840s boundary): By the mid-19th century, policy moved toward restricting who could issue notes and under what conditions; the Bank Charter Act (1844) is the landmark statute that formalized this direction.

Trust and governance (why anyone accepted it)

- Credibility through institutional commitment: A suspension can be stable if markets believe the state and the central bank will preserve acceptability and return to convertibility. A detailed historical study argues that Bank of England notes were accepted at face value throughout 1797–1821 and that expectations of resumption strengthened after Waterloo.

- Crisis behavior as reputation-building: The Bank’s willingness to lend against collateral during panics (even at risk to itself) gradually built a reputation that supported systemic confidence—especially after episodes like 1825.

- Legal constraint as trust technology: Regulation of note issuance (who may issue, under what limits) functions as a governance layer to reduce the probability of destabilizing over-issuance and runs.

Revenue model (who made money from the system)

- Banks (private and central): Earned via discounting bills, making advances, and (where permitted) capturing spreads between funding costs and lending returns. In crisis, the same channels double as stability tools.

- States: Benefited from wartime finance capacity during suspension regimes; suspending convertibility reduced immediate gold-drain constraints on note issuance during conflict.

- Provincial issuers: Country banks profited by issuing notes and expanding credit locally, but the model carried higher run risk—prompting reform pressure after crises.

Failure modes and constraints

- Runs and liquidity spirals: When holders doubt convertibility or asset quality, they rush to convert or withdraw, forcing banks to liquidate assets and amplifying panic—visible in 1825’s escalation and emergency response.

- Governance drift: Even strong systems can fail if institutional discipline erodes; modern central-bank research uses the Bank of Amsterdam’s long-run arc as a cautionary case for governance/credibility limits (a relevant comparator for this epoch’s “paper credibility” problem).

- Fragmented issuance: Many independent note issuers increase systemic opacity and instability risk—explicitly criticized in parliamentary debate.

What scaled it (the scaling technology)

- Paper liabilities + acceptance networks: Notes made payments scalable even when coin was scarce or costly to transport.

- Discounting infrastructure (bills of exchange as liquidity collateral): Central-bank discount windows and bill markets enabled rapid liquidity provision in stress.

- Institutional rulemaking (note-issue limits, branch networks): Stability improved when issuance became more centralized/regulated and distribution networks expanded.

Caption:

“Paper scaled payments, but stability required credibility: convertibility rules, crisis lending, and tighter note-issue governance.”

Sources

- Bank of England — “History” (Restriction Period 1797–1821; suspension of gold payments).

- Bank Underground (Bank of England) — “War and payment innovation: the adoption of paper currency in Britain” (1797 suspension context).

- Newby (2007, University of St Andrews working paper) — “The Suspension of Cash Payments as a Monetary Regime” (credibility and acceptance during 1797–1821).

- Fulmer (2022) — “The Bank of England’s Lending during the Panic of 1825” (quantified discounts/advances; de facto LOLR behavior).

- Bank of England Quarterly Bulletin (1965) — “The note circulation” (1826 branches; 1844 note-issue constraints).

- UK Legislation — Bank Charter Act 1844 (text and purpose: regulate note issue).

- Hansard (1826) — Parliamentary debate on country bank note issuance and systemic consequences.

- Sveriges Riksbank — Historical timeline (1661 first European banknotes; failure; context for paper credibility).

- Sveriges Riksbank — “Sveriges Riksbank and the History of Central Banking” (historical comparisons across central banks).