Post-Crisis Money and Platform Payments: QE, Instant Rails, Open Banking, Crypto/Stablecoins, and CBDC (2008–2025)

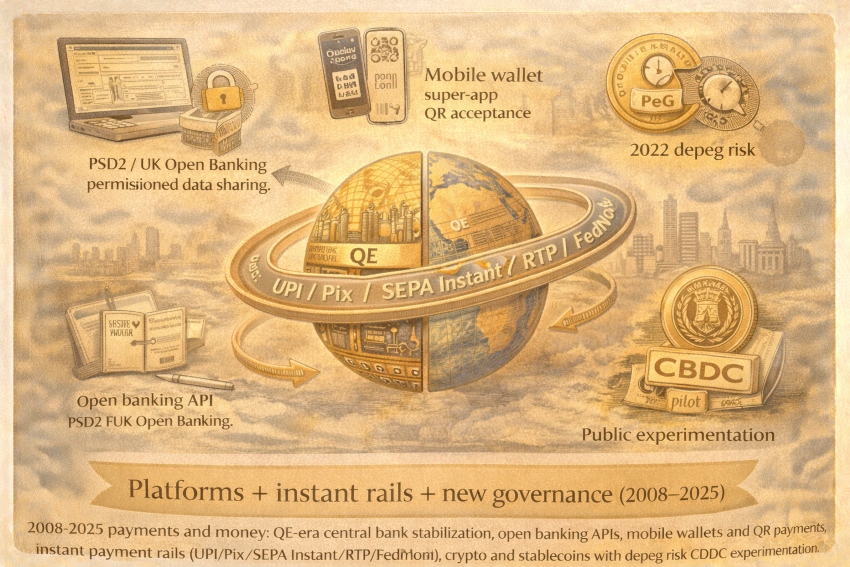

“2008–2025 payments and money: QE-era central bank stabilization, open banking APIs, mobile wallets and QR payments, instant payment rails (UPI/Pix/SEPA Instant/RTP/FedNow), crypto and stablecoins with depeg risk, and CBDC experimentation.”

Summary of events during the period

From 2008 to 2025, the “story of money” is less about new coins and more about new operating regimes: (1) central banks using balance sheets at scale (QE/QT), (2) a regulatory reset to harden banks and markets after 2007–09, (3) the rise of platform-mediated retail payments (mobile wallets, QR, super-app ecosystems), (4) the build-out of instant account-to-account rails, and (5) the parallel emergence of crypto rails and stablecoins, triggering a second wave of rule-making and state experiments (CBDCs). The period is defined by repeated stress tests—COVID-era liquidity shock, crypto blowups, and the 2023 banking stress—followed by fast innovation in rails and governance.

Payment media (what people used to pay)

- Deposits remain dominant: most payments are still “account money,” but increasingly initiated through apps, wallets, and APIs rather than paper instruments.

- Central bank money becomes “system lubricant” at scale: the Fed’s first LSAP/QE round (late 2008–2010) included very large MBS and agency debt purchases—illustrating how central bank balance sheets became a primary stabilization tool.

- Mobile wallets and tokenized cards: Apple Pay’s U.S. launch (Oct 2014) exemplifies the move to phone-based credentials layered on top of card networks.

- QR-based platform money at national scale (China): research notes Alipay and WeChat Pay introduced proprietary QR approaches around 2011 and, by 2016, QR transactions reached very large volumes—showing how payment acceptance can scale via software + platforms rather than POS hardware.

- Cryptoassets and stablecoins as parallel “settlement media”: the Bitcoin design (2008) seeded a new class of bearer-style digital assets; Ethereum (2015) enabled programmable money and DeFi primitives.

- CBDC as state response/exploration: the Atlantic Council tracker reports 137 jurisdictions exploring CBDCs and identifies a small number of live retail CBDCs (e.g., Bahamas, Jamaica, Nigeria).

How prices were set (negotiated vs administered vs regulated)

Negotiated (market pricing)

- Most goods/prices remain market-set, but payment choice increasingly affects effective prices via discounts, rewards, fees, and embedded credit (BNPL, installments, wallet incentives).

Administered/regulated (fee and access rules)

- Payment pricing is often rule-driven: network fees, wallet terms, and platform governance. In the EU, interchange fee regulation caps consumer card interchange (0.2% debit, 0.3% credit), directly shaping the economics of card acceptance.

Macro “price of money” set by policy regimes

- Post-2008, the stance of monetary policy is increasingly implemented through interest-rate policy plus balance-sheet tools (QE/QT). The Fed’s published balance-sheet timeline documents the 2008–09 LSAP decisions and magnitudes.

How payments cleared (the “rails”)

- Instant account-to-account rails spread globally

- UK Faster Payments (2008) is an early national model for near-real-time retail transfers.

- UPI (India): Digital India documents a pilot launch on 11 April 2016, showing how interoperable instant payments can scale via standardized addressing and bank connectivity.

- RTP (U.S., 2017): The Clearing House states its RTP network launched in 2017 to bring instant payments to the United States.

- SEPA Instant (EU, Nov 2017): ECB/EPC sources describe SCT Inst as the basis for euro instant credit transfers, launched in November 2017.

- Pix (Brazil, live 16 Nov 2020): the Central Bank of Brazil describes Pix as performing instant transfers since 16 November 2020.

- FedNow (U.S., July 2023): the Federal Reserve announced and then launched FedNow as an instant payments service.

- Open banking becomes a payments “layer”

- PSD2 (EU) and UK Open Banking institutionalize API-based access/competition: PSD2 transposition deadline 13 Jan 2018; UK Open Banking launch 13 Jan 2018.

- Messaging modernization (ISO 20022)

- Riksbank notes the Eurosystem’s migration to ISO 20022 in March 2023 and expects global transition to continue until 2025; SWIFT describes March 2023 as a milestone starting the ISO 20022 CBPR+ migration.

Trust and governance (why anyone accepted it)

- Post-crisis bank hardening (Basel III, 2010 onward): BIS describes Basel III as a global framework for stronger capital and liquidity standards, endorsed by G20 leaders, reflecting the “never again” governance response to 2007–09.

- U.S. supervisory and consumer reform (Dodd-Frank, 2010): the Fed’s historical summary notes Dodd-Frank was signed July 21, 2010 and aimed at correcting crisis causes and strengthening oversight.

- Crisis backstops remain central: in March 2023 the Fed created the Bank Term Funding Program (BTFP), lending up to one year against eligible collateral valued at par—illustrating how “trust” still depends on credible liquidity support.

- Crypto governance converges toward “same risk, same regulation”

- The FSB issued a global regulatory framework (July 2023) for crypto-asset activities and markets.

- The EU’s MiCA entered into force in 2023, with stablecoin (ART/EMT) provisions applying from 30 June 2024 and broader CASP requirements from 30 December 2024 (per EU authorities).

Revenue model (who made money from the system)

- Platforms and wallets: monetization via merchant acquiring economics, wallet distribution leverage, and data-driven ecosystem “stickiness” (offers, loyalty, identity).

- Card networks and issuers: still collect network fees and interchange-related economics, though fee caps in some jurisdictions compress pricing power.

- Banks and instant-rail operators: monetization via value-added services (fraud controls, overlays like request-to-pay, business invoicing, treasury tools) rather than per-transaction “tolls.”

- Stablecoin issuers and crypto intermediaries: earn via reserve yield (where applicable), issuance/redemption fees, trading, custody, and on-chain infrastructure—under increasing regulatory constraints.

Failure modes and constraints

- Macro-financial fragility does not disappear: post-2008 tools stabilized markets, but new stress episodes required new facilities (e.g., 2023 BTFP).

- Platform concentration and rule risk: when acceptance, wallet access, or API terms change, merchants and consumers experience “governance shocks” even without a macro crisis.

- Stablecoin “peg” risk and reflexive spirals: the Terra/UST episode (May 2022) is widely analyzed as triggered by a stablecoin depeg with large spillovers; Reuters reported spillovers across the crypto market during the collapse window.

- Interoperability and fragmentation: parallel real-time systems can reduce network effects if they do not interoperate (a recurring adoption question in many markets).

What scaled it (the scaling technology)

- Balance-sheet policy + swap/liquidity facilities as “infrastructure for trust” during shocks.

- Instant payments as a public/utility rail (UPI, Pix, SEPA Instant, RTP, FedNow) enabling 24/7 settlement and new overlays.

- Open banking APIs turning bank accounts into programmable endpoints for fintech and merchants.

- Standardized messaging (ISO 20022) enabling richer data, compliance automation, and higher straight-through processing globally.

- Programmable rails (smart contracts) enabling stablecoins, DeFi, and tokenized financial products—followed by rapid regulatory formalization.

Caption:

“After 2008, trust scaled through central bank backstops and stronger rules—while everyday payments shifted to platforms, instant rails, and programmable money.”

Sources

- Monetary policy & crisis backstops

- Federal Reserve — Timeline: Balance Sheet Policies (LSAP/QE decisions, 2008–09). :contentReference[oaicite:30]{index=30}

- New York Fed — Large-Scale Asset Purchases (LSAP program details, 2008–10). :contentReference[oaicite:31]{index=31}

- Federal Reserve History — Great Recession and Its Aftermath (LSAP purpose and context). :contentReference[oaicite:32]{index=32}

- Federal Reserve — Bank Term Funding Program (BTFP terms and collateral at par). :contentReference[oaicite:33]{index=33}

- Post-crisis regulation

- BIS — Basel III rules text (Dec 2010; endorsed by G20; capital & liquidity framework). :contentReference[oaicite:34]{index=34}

- Federal Reserve History — Dodd-Frank Act (signed July 21, 2010; reform overview). :contentReference[oaicite:35]{index=35}

- Instant payments (global)

- UK Faster Payments launch date (industry reference). :contentReference[oaicite:36]{index=36}

- Digital India — UPI pilot launch on 11 April 2016. :contentReference[oaicite:37]{index=37}

- The Clearing House — RTP launched in 2017. :contentReference[oaicite:38]{index=38}

- ECB — Instant payments based on SCT Inst (launched Nov 2017). :contentReference[oaicite:39]{index=39}

- EPC — SCT Inst press kit (Nov 2017 launch). :contentReference[oaicite:40]{index=40}

- Central Bank of Brazil — Pix instant transfers since 16 Nov 2020. :contentReference[oaicite:41]{index=41}

- Federal Reserve — FedNow July 2023 launch announcement and launch page. :contentReference[oaicite:42]{index=42}

- Open banking & payment rules

- EUR-Lex — PSD2 (Directive (EU) 2015/2366) / transposition deadline 13 Jan 2018 (EU Parliament brief). :contentReference[oaicite:43]{index=43}

- Open Banking (UK) — Launch on 13 Jan 2018. :contentReference[oaicite:44]{index=44}

- EUR-Lex summary — Interchange Fee Regulation caps (0.2% debit, 0.3% credit). :contentReference[oaicite:45]{index=45}

- Messaging modernization

- Sveriges Riksbank — Eurosystem ISO 20022 migration March 2023; global transition expected until 2025. :contentReference[oaicite:46]{index=46}

- SWIFT — CBPR+ ISO 20022 migration milestone (March 2023). :contentReference[oaicite:47]{index=47}

- Platforms & wallets; crypto/CBDC governance

- Apple — Apple Pay available starting Oct 20, 2014 (launch announcement). :contentReference[oaicite:48]{index=48}

- CGAP — China digital payments: Alipay/WeChat Pay QR codes (2011) and 2016 volume figure. :contentReference[oaicite:49]{index=49}

- Bitcoin.org — “Bitcoin: A Peer-to-Peer Electronic Cash System” (white paper). :contentReference[oaicite:50]{index=50}

- Ethereum.org — Ethereum launched July 30, 2015. :contentReference[oaicite:51]{index=51}

- FSB — Global Regulatory Framework for Crypto-asset Activities (July 2023). :contentReference[oaicite:52]{index=52}

- EU MiCA applicability dates (ART/EMT from 30 June 2024; CASPs from 30 Dec 2024). :contentReference[oaicite:53]{index=53}

- Atlantic Council — CBDC Tracker (global exploration numbers; launched CBDCs list). :contentReference[oaicite:54]{index=54}

- Terra/UST depeg and spillovers (academic + contemporaneous reporting). :contentReference[oaicite:55]{index=55}