Financial Globalization and Digital Market Infrastructure: Cards, RTGS, Securitization, and the 2008 Shock (c. 1980–2008)

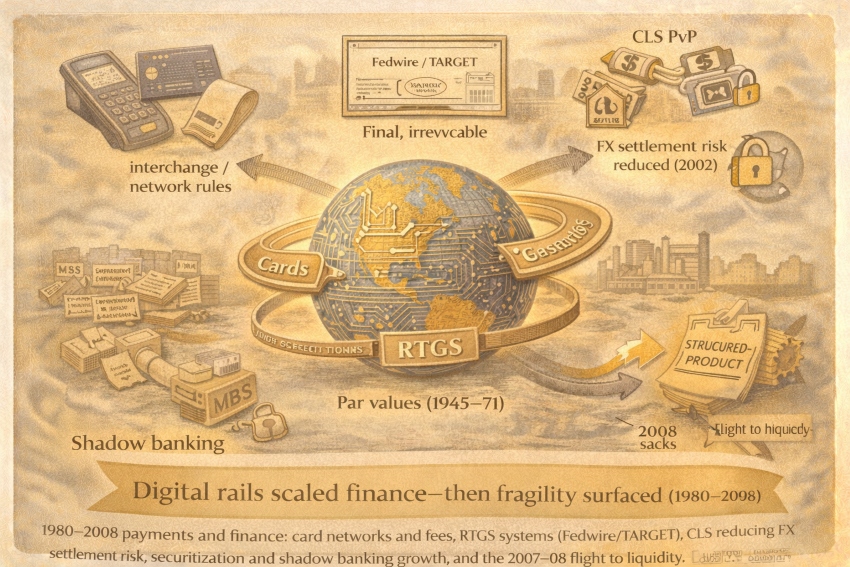

“1980–2008 payments and finance: card networks and fees, RTGS systems (Fedwire/TARGET), CLS reducing FX settlement risk, securitization and shadow banking growth, and the 2007–08 flight to liquidity.”

Summary of events during the period

From roughly 1980 to 2008, money and payments scaled less through new “forms of currency” and more through market infrastructure: electronic retail payment networks (cards and direct transfers), wholesale real-time settlement systems, and globally integrated banking and capital markets. In parallel, deregulation and regulatory harmonization enabled financial firms to expand product scope and balance sheets, while securitization and “market-based” (shadow) intermediation grew rapidly. The era’s signature ending was the 2007–08 crisis, when doubts about structured mortgage products triggered a funding run on parts of the shadow banking system and forced central banks and governments into extraordinary stabilization.

Payment media (what people used to pay)

- Card payments at mass scale (credit/debit): Across advanced economies, the late-20th-century trend is sustained growth in payment cards and non-cash retail payments, even as cash remains important for face-to-face volume.

- Bank deposits as the dominant “money for scale”: Most high-frequency commerce runs on deposit money (account balances), with consumer payments increasingly “credential-based” (card credentials) rather than cash-based.

- Early online payments (late 1990s): The rise of internet commerce created demand for online payment intermediaries; PayPal traces back to Confinity (1998) and launched an early digital wallet/payment product in 1999.

- Securitized claims as quasi-money in wholesale finance: By the 2000s, many institutions financed assets through markets using securitized products and short-term funding structures—creating money-like liabilities outside traditional deposit banking.

How prices were set (negotiated vs administered vs regulated)

Negotiated prices (markets)

- Consumer prices, wages, and most asset prices remained market-set. What changed was market microstructure: faster execution, easier comparison, and global capital mobility increased price responsiveness.

Administered and regulated components (fees, rules, and capital constraints)

- In card markets, “what it costs to pay” is partly governed by network rules and fee structures, especially interchange fees and scheme rules—topics central banks and regulators explicitly study and sometimes challenge.

- Prudential regulation shaped the price of risk by constraining bank leverage. Basel I (1988) established risk-weighted capital requirements (with the well-known 8% minimum ratio), while Basel II (2004) expanded risk sensitivity and formalized the three-pillar approach (minimum capital, supervisory review, market discipline).

- U.S. structural regulation also shifted: the Gramm–Leach–Bliley Act (1999) repealed major parts of Glass–Steagall separation, enabling broader financial holding company structures.

How payments cleared (the “rails”)

- RTGS for large-value payments: The modern backbone is real-time gross settlement where transfers are final and irrevocable once processed; the Fedwire Funds Service is explicitly described this way by the Federal Reserve.

- European monetary integration rails: With the euro’s launch, TARGET went live on 4 January 1999 as the first-generation Eurosystem RTGS linking national systems for cross-border euro payments.

- FX settlement risk reduction (CLS, 2002): A key wholesale upgrade was payment-versus-payment FX settlement. CLS began operations in September 2002 to reduce (“largely eliminate”) FX settlement risk, a goal emphasized by central banks and the BIS.

- Retail network clearing at scale: Card networks, ACH-like batch systems, and direct credit/debit transfers scaled consumer and business payments; BIS comparative work documents broad cross-country trends toward more card use and direct funds transfers.

Trust and governance (why anyone accepted it)

- Network trust (payments): Retail systems depend on technical reliability, fraud controls, and rule enforcement (chargebacks, authentication, dispute processes). Governance is partly private (network rules) and partly public (consumer protection, competition scrutiny).

- Prudential trust (banks): Basel capital standards function as credibility technology—aimed at ensuring banks can absorb losses and remain solvent; Basel II explicitly builds on Basel I with expanded risk measurement and supervisory architecture.

- Systemic trust (market-based finance): Shadow banking grew as a “market-based financial system” performing maturity/liquidity transformation without the same official backstops as banks, as described in the NY Fed’s foundational work on shadow banking.

Revenue model (who made money from the system)

- Card networks, issuers, and acquirers: Revenue comes from merchant service charges, interchange-related economics, and network fees—often debated as part of the interchange fee policy discussion.

- Banks and broker-dealers: Earned via lending spreads, underwriting, market-making, securitization fees, and balance-sheet intermediation—amplified by global capital mobility and product expansion.

- Online payment intermediaries: Monetized e-commerce growth by providing checkout, fraud screening, and merchant aggregation (e.g., PayPal’s early model as a digital wallet/payment processor).

Failure modes and constraints

- Model risk and opacity in securitization: The subprime mortgage boom relied heavily on funding mortgages via repackaging into securities sold to investors; the Federal Reserve’s historical account highlights private-label MBS as a major funding channel for subprime lending.

- Run dynamics in shadow banking (2007–08): BIS analysis describes a “flight to liquidity and safety” beginning in 2007 as doubts about mortgage-backed securities rose and the shadow banking system began contracting—propagating stress internationally.

- Systemic risk from nonbank maturity transformation: The IMF and FSB emphasize that shadow banking can support credit and liquidity, but also carries bank-like risks that became evident during the 2007–08 crisis, including fire-sale spirals and abrupt credit contraction.

What scaled it (the scaling technology)

- Electronic credentials + networks (retail): Cards and direct transfers scale because authentication and clearing are networked; growth in cards and direct transfers is documented as a common cross-country trend.

- RTGS and global settlement utilities (wholesale): Fedwire-style RTGS provides finality; TARGET integrated euro settlement; CLS reduced FX settlement risk with PvP mechanics.

- Regulatory harmonization (prudential): Basel I and Basel II standardized key dimensions of bank capital governance across borders, shaping how large institutions priced and allocated risk.

- Securitization + market-based funding: Enabled rapid credit expansion but also created fragility when confidence in collateral and structures collapsed.

Caption:

“Networks and market infrastructure scaled payments and credit—until securitization opacity and shadow funding run-risk triggered the 2007–08 crisis.”

Sources

- BIS/CPMI (2001): Retail payments in selected countries: a comparative study (cash primacy + growth in cards and direct transfers).

- Federal Reserve (Fedwire Funds Service): RTGS; immediate, final, irrevocable once processed.

- ECB: TARGET launch (4 Jan 1999) and TARGET history as Eurosystem RTGS.

- BIS Quarterly Review (2002): CLS Bank began operation in September 2002 to reduce FX settlement risk.

- Bundesbank: CLS oversight page confirming operations began 9 Sep 2002 and purpose (settlement risk/Herstatt risk).

- BIS (1988 text): Basel Capital Accord (minimum capital standards; Basel I).

- BIS (2004): Basel II: International Convergence of Capital Measurement and Capital Standards (framework).

- Federal Reserve History: Gramm–Leach–Bliley Act (1999) repealed large parts of Glass–Steagall.

- FRASER (St. Louis Fed): Full text of GLBA showing Glass–Steagall repeal provisions.

- NY Fed Staff Report (Pozsar et al., 2010): Definition and mechanics of shadow banking; growth since mid-1980s.

- BIS Working Paper (2011): 2007 doubts about MBS → contraction of shadow banking; flight to liquidity.

- Federal Reserve History: Subprime mortgage crisis—funding via repackaging into securities; role of private-label MBS.

- IMF GFSR (2014) chapter: Shadow banking risks visible in 2007–08.