War, Depression, Controls, and the Birth of the Modern Monetary Order (1914–1945)

“1914–1945 monetary transformation: collapse of gold-standard discipline, war bonds, interwar hyperinflation, capital and exchange controls, WWII rationing and price controls, and Bretton Woods institution-building.”

Summary of events during the period

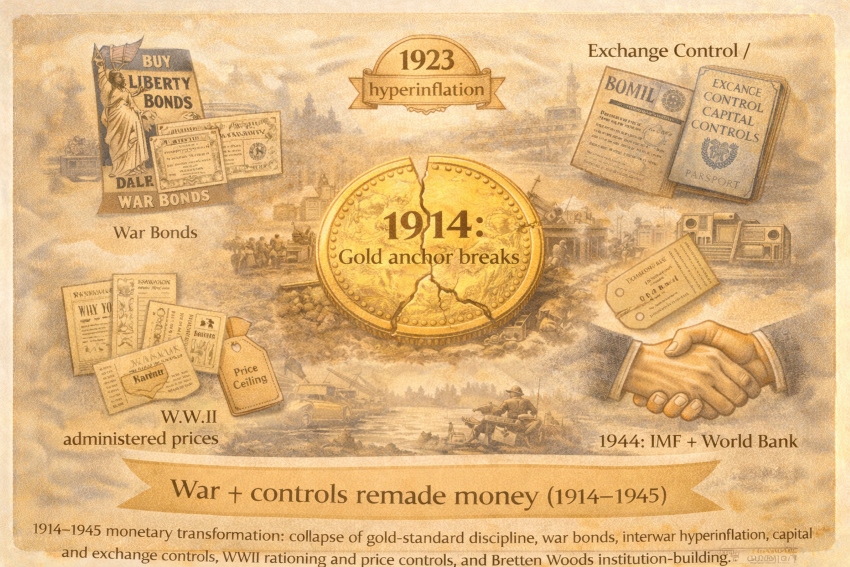

From 1914 to 1945, the monetary world shifted from a gold-anchored, market-integrated system to a regime defined by wartime finance, monetary experimentation, capital and exchange controls, and (by 1944–45) a deliberate effort to design a new international order. World War I triggered a broad breakdown of pre-1914 gold standard practices; the interwar years saw an attempted restoration via the gold-exchange standard, punctuated by hyperinflations and then the Great Depression; the 1930s brought widespread currency realignments, capital controls, and trade/currency blocs; and World War II pushed states into comprehensive management of rates, prices, and allocations. The period ends with the Bretton Woods Conference (July 1944) establishing the IMF and World Bank as pillars of postwar monetary cooperation.

Payment media (what people used to pay)

- Notes and deposits scale rapidly under war finance: War spending pushes economies toward bank money (notes + deposits), because coin and gold are insufficient for the fiscal scale required.

- Government war bonds as mass finance instruments: In the U.S., WWI “Liberty Bonds” were sold via multiple drives and raised on the order of $17 billion, with taxes providing a smaller share of total war funds—illustrating how retail debt sales became a core funding channel.

- Gold’s role shifts from everyday anchor to controlled strategic asset: By 1933–34, the U.S. sharply limited private gold use and centralized gold in the Treasury via Executive Order 6102 and the Gold Reserve Act—representative of a broader move toward managed gold policies.

- Ration stamps and controlled purchasing power (WWII): During WWII, payment for some goods required not only money but also ration points/stamps, effectively creating a dual-key purchase system (money + authorization).

How prices were set (negotiated vs administered vs regulated)

Negotiated prices (where markets still functioned)

- Many goods still cleared through bargaining/competition, but the “normal” price mechanism was repeatedly disrupted by shocks (mobilization, shortages, supply chain disruption, and monetary instability).

Administered prices (wartime price ceilings)

- WWII saw explicit, large-scale price administration. In the U.S., the Office of Price Administration (OPA) was created in 1941 and subsequently had authority to impose price ceilings and ration scarce goods; rationing reinforced price controls by limiting demand.

Regulated prices via monetary regime choices

- Under gold-standard rules, “the price of money in gold” is governed by convertibility commitments. When countries left gold (1931 UK; 1933 US), currency value and domestic price levels became more directly shaped by policy choices and controls. Britain’s 1931 exit is documented in official Treasury statements preserved by the UK National Archives.

How payments cleared (the “rails”)

- 1914 shock → gold anchor breaks: After WWI began, most countries left the gold standard; exchange rates floated more, and inflation rose—shifting clearing from gold-parity discipline to wartime policy regimes.

- Interwar attempt to rebuild the “gold rail”: The 1920s restoration effort often operated as a gold-exchange standard (reserves held partly in key currencies convertible to gold), with credibility problems that research links to instability and eventual breakdown.

- 1930s: clearing constrained by capital controls and blocs: In response to banking crises, reserve losses, and capital flight—especially around 1931—many European countries adopted capital controls; NBER research treats this as the first widespread crisis-era use of controls and analyzes how they affected stabilization and recovery.

- 1936: partial coordination via the Tripartite Agreement: The U.S., UK, and France issued a stabilization declaration in September 1936 (primary text preserved by Yale’s Avalon Project), aiming to reduce destructive currency conflict after the early-1930s monetary breakdown.

- WWII: state-directed clearing (rates + allocation): In the U.S., the Federal Reserve adopted wartime interest-rate pegs at Treasury request in 1942, including a 3/8% bill rate and an effective cap on long-term bond yields around 2.5%, explicitly to support cheaper war finance—an archetype of financial repression.

Trust and governance (why anyone accepted it)

- Credibility can be destroyed quickly (hyperinflation)

- Germany’s 1922–23 hyperinflation is widely described as rooted in war-finance debt burdens and triggered/intensified by the 1923 Ruhr occupation and passive resistance, with the state financing obligations through money creation—destroying the unit of account and forcing a stabilization/reset.

- IMF materials treat the episode as a canonical hyperinflation/stabilization case in modern monetary history.

- Credibility can be manufactured through rules + coercion

- Wartime price controls/rationing and interest-rate pegs effectively substitute administrative credibility for market credibility: the state enforces acceptance (ration rules; controlled borrowing costs; exchange restrictions).

- Institutional redesign becomes the governance solution

- Bretton Woods (July 1944) reflects an explicit governance response: creating shared institutions (IMF/World Bank) to reduce destructive interwar dynamics and stabilize postwar settlement.

Revenue model (who made money from the system)

- States: financed war primarily via a blend of taxation + bond sales, often leaning heavily on debt. WWI Liberty Bond drives illustrate mass retail debt placement; WWII repeats the model at larger scale.

- Banks/central banks: intermediated government finance and managed liquidity; wartime pegging explicitly lowered state borrowing costs while shifting risk onto the monetary authority’s balance sheet.

- Private actors: profited in channels that remained market-based (procurement, black markets where controls bit, foreign exchange arbitrage where legal constraints created premia).

Failure modes and constraints

- Hyperinflation and unit-of-account collapse: When fiscal obligations are funded by money creation under severe stress, the currency can cease to function as a store of value and pricing becomes chaotic (Weimar is the archetype).

- Gold-standard rigidity under depression: Research and historical synthesis emphasize that attempts to maintain gold convertibility could amplify deflationary pressure; exits (e.g., 1931 UK) often became turning points in domestic policy freedom.

- Capital flight and reserve loss: The 1931 crisis wave shows how fast cross-border finance can destabilize fixed regimes—prompting widespread adoption of capital controls.

- Control regimes breed distortions: Price controls and rationing can stabilize official prices but tend to create shortages, queuing, and black-market incentives—hence the heavy administrative apparatus required.

What scaled it (the scaling technology)

- Mass retail sovereign debt distribution (bond drives): A scalable way to move household savings into wartime finance.

- Exchange and capital controls: Scaled “defensive monetary sovereignty” by limiting destabilizing flows when credibility was fragile.

- Financial repression toolkit (rate pegs + captive demand): WWII interest-rate caps show how states scaled cheap funding by managing the yield curve.

- Institutional architecture (Bretton Woods): Scaling postwar settlement and cooperation through the IMF/World Bank framework.

Caption:

“From gold to management: wars and depression drove bond finance, controls, and a redesigned postwar monetary order.”

Sources

- Sveriges Riksbank (timeline): “1914 – The gold standard collapses” (WWI outbreak; most countries leave gold; rates float; inflation rises). :contentReference[oaicite:25]{index=25}

- Federal Reserve History: “Liberty Bonds” (WWI bond drives; ~$17B raised; bonds vs taxes). :contentReference[oaicite:26]{index=26}

- The American Presidency Project (UC Santa Barbara): Executive Order 6102 (April 5, 1933) text. :contentReference[oaicite:27]{index=27}

- Federal Reserve History: “Gold Reserve Act” (Jan 30, 1934; culmination of gold program). :contentReference[oaicite:28]{index=28}

- UK National Archives (primary source): Treasury press statement on leaving the gold standard (Sept 20, 1931). :contentReference[oaicite:29]{index=29}

- NBER Working Paper (Bordo & MacDonald, 2001): “The Inter-War Gold Exchange Standard: Credibility and …” :contentReference[oaicite:30]{index=30}

- NBER Working Paper (Eichengreen, 1993): “Trade blocs, currency blocs and the …” (1930s regionalization and policy). :contentReference[oaicite:31]{index=31}

- NBER Working Paper (Mitchener & Wandschneider, 2014): “Capital Controls and Recovery…” (1931 crisis; capital flight; controls). :contentReference[oaicite:32]{index=32}

- Yale Avalon Project (primary source): “Monetary Stabilization; September 25, 1936” (Tripartite Agreement declaration text). :contentReference[oaicite:33]{index=33}

- Federal Reserve History: “The Treasury–Fed Accord” (WWII interest-rate peg details beginning 1942). :contentReference[oaicite:34]{index=34}

- Chicago Fed Economic Perspectives (2021): “Yield Curve Control in the United States, 1942–1951” (WWII peg and caps). :contentReference[oaicite:35]{index=35}

- Britannica (Germany/Weimar): “Years of crisis 1920–23” (root and trigger of 1923 hyperinflation; Ruhr occupation). :contentReference[oaicite:36]{index=36}

- Britannica (Weimar Republic): “The Ruhr and inflation” (passive resistance context). :contentReference[oaicite:37]{index=37}

- IMF eLibrary (historical chapter): references on “The 1923 Hyperinflation and Stabilization” (canonical case framing). :contentReference[oaicite:38]{index=38}

- U.S. Government (GovInfo PDF): “Rationing in World War II” (rationing reinforced price controls). :contentReference[oaicite:39]{index=39}

- National WWII Museum: “Rationing during WWII” (ration points/stamps + money). :contentReference[oaicite:40]{index=40}

- Federal Reserve History: “Creation of the Bretton Woods System” (July 1944; IMF + World Bank). :contentReference[oaicite:41]{index=41}

- IMF Factsheet: “The IMF and the World Bank” (created July 1944 at Bretton Woods). :contentReference[oaicite:42]{index=42}

- World Bank Archives: “Bretton Woods and the Birth of the World Bank” (conference begins July 1, 1944; context). :contentReference[oaicite:43]{index=43}