Industrial-Age Payments: Cheques, Clearinghouses, Telegraph Transfers, and the Classical Gold Standard (c. 1840–1914)

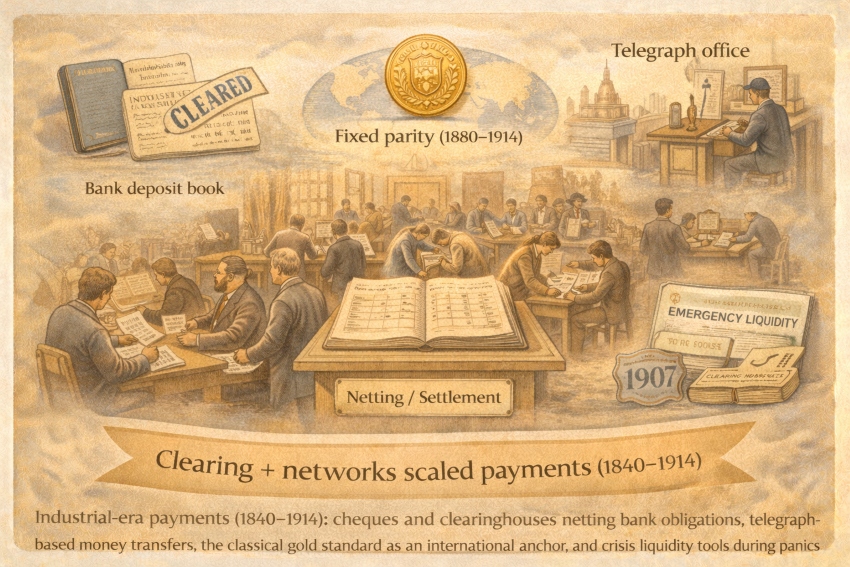

“Industrial-era payments (1840–1914): cheques and clearinghouses netting bank obligations, telegraph-based money transfers, the classical gold standard as an international anchor, and crisis liquidity tools during panics.”

Summary of events during the period

From roughly 1840 to 1914, the decisive scaling move in payments was the shift from “coin-handling” toward institutional clearing. Retail life still used coins and notes, but high-volume commerce increasingly cleared through deposit banking + cheques, with obligations netted at clearinghouses rather than settled one-by-one in cash. This clearing architecture expanded geographically (inter-city and national networks), and technologically (telegraph-based money transfer). At the international level, the “classical gold standard” (roughly 1880–1914) provided a widely shared settlement anchor through fixed gold parities and convertibility rules—supporting predictable exchange rates while leaving domestic systems exposed to liquidity stress and periodic panics.

Payment media (what people used to pay)

- Cheques and deposits (bank money): The 19th century is the breakout period for cheque-based payments, which scale because they use bank deposits as the underlying medium and rely on clearing to settle between banks.

- Clearinghouse settlement assets (reserves/specie certificates): Clearinghouses reduce the amount of “final settlement” asset banks must hold by netting obligations multilaterally, which becomes increasingly formalized in the 19th century (e.g., London multilateral settlement from 1841).

- Telegraph-based remittances (“wire” transfers): By the late 19th century, telegraph networks supported money transfer services—most famously Western Union’s consumer money transfer service introduced in 1871 (sending instructions by telegraph so funds could be paid out at another office).

- Gold as the ultimate international settlement anchor: Under the classical gold standard, currencies were defined in terms of gold (or linked to a gold currency), and convertibility rules underpinned fixed exchange rates for much of 1880–1914.

How prices were set (negotiated vs administered vs regulated)

Negotiated pricing (market level)

- Most goods and wages were priced through bargaining and competitive market conditions; what changed was not the existence of negotiation, but the speed and integration of markets as payments and information moved faster (clearing networks and telegraph communication).

Administered anchors (gold parity as macro “price rule”)

- Gold-standard adherence effectively set a “macro price rule” for currency value: authorities committed to a fixed gold parity and convertibility conventions, shaping domestic monetary conditions through the constraints of maintaining that parity.

Regulation through settlement rules and note/bank governance

- Clearinghouses and central banks shaped the economic environment by setting participation rules, reserve practices, and crisis arrangements—governing how quickly and safely obligations could be settled at scale.

How payments cleared (the “rails”)

- Multilateral clearing (London as a model): As payment volumes rose, banks moved from bilateral settling toward multilateral netting; scholarship on interbank settlement explicitly notes the London clearinghouse settling multilaterally from 1841 onwards.

- National clearinghouses (United States, 1853 onward): The New York Clearing House, founded in 1853, rationalized interbank settlement in a rapidly growing banking center—creating a private infrastructure that later behaved like a quasi-central bank in crises.

- Telegraph transfer rails (late 19th century): Telegraph remittance worked as an operational rail for long-distance payments: the sender deposited funds at a telegraph office; a message authorized payout elsewhere, typically controlled via identifiers/passwords.

- Crisis clearing innovations (1907): During the Panic of 1907, clearinghouse associations issued collateralized instruments (clearinghouse loan certificates) and used coordinated restrictions/arrangements to preserve cash and stabilize settlement—an explicit precursor to modern emergency liquidity tools.

Trust and governance (why anyone accepted it)

- Clearinghouse governance as trust technology: Netting only works if members trust the rules, audits, and settlement discipline. Historical studies of payment systems emphasize that rising scale pushed clearing arrangements to become more formalized and rules-based.

- Central-bank crisis doctrine (Bagehot, 1873): The lender-of-last-resort principle—lend freely to solvent firms, against good collateral, at a high/penalty rate—was articulated by Walter Bagehot in 1873 and remains a defining rule-set for crisis credibility.

- Gold-standard credibility: The gold anchor functioned when markets believed convertibility rules were real and sustainable; central-bank and treasury behavior therefore became part of the monetary “trust surface.”

Revenue model (who made money from the system)

- Commercial banks: Earned from intermediation (loan/deposit spreads), payment services, and correspondents—benefiting directly from cheque adoption and clearing efficiencies. (The expansion of cheque clearing is treated as a major cost-reduction and scale mechanism in historical work on cheque evolution.)

- Telegraph money transmitters: Monetized long-distance remittances through fees—Western Union explicitly promoted and expanded consumer-to-consumer transfers once the telegraph network made it operationally feasible.

- States and central banks: Benefited from improved fiscal and financial stability capacity when gold-standard credibility held and when crisis mechanisms prevented destructive collapses (even if the details varied country by country).

Failure modes and constraints

- Liquidity panics inside “efficient” rails: Cheques and deposits scale payments, but they also increase the system’s dependence on confidence. Panics can force payment suspensions unless a credible liquidity backstop exists—illustrated sharply by 1907’s emergency clearinghouse actions.

- Gold-standard rigidity under stress: Fixed parity systems can transmit shocks through gold flows and reserve constraints; historical discussions of the gold era emphasize formal convertibility rules and the scarcity of gold as a constraint.

- Institutional gaps (U.S. before 1913): Repeated banking panics and “inelastic currency” concerns were central motivations behind creating the U.S. Federal Reserve in 1913.

What scaled it (the scaling technology)

- Clearinghouses (netting at scale): Multilateral clearing reduces settlement-asset needs and operational costs, enabling a large rise in transaction volumes without proportional increases in cash handling.

- Telegraph-enabled transfers: Payments could move as authenticated messages rather than transported metal—an early form of remote authorization and payout.

- A shared international settlement anchor (1880–1914): The classical gold standard provided a widely used coordination mechanism for exchange rates and cross-border settlement during the pre-WWI global trade expansion.

- Central-bank crisis doctrine and institutions: Bagehot-style crisis lending principles, combined with evolving institutions, reduced the probability that liquidity shocks would become full systemic breakdowns—though not eliminating panics.

Caption:

“Industrial economies scaled by shifting settlement from moving cash to clearing obligations—backed by gold-standard credibility and evolving crisis tools.”

Sources

- Boel, P. (2019). “Payment systems – historical evolution and literature review” (Sveriges Riksbank). https://www.riksbank.se/globalassets/media/rapporter/pov/artiklar/engelska/2019/190613/er-2019_1-payment-systems–historical-evolution-and-literature-review.pdf

- Norman, B. (2011). “The history of interbank settlement arrangements…” (ECB Working Paper No. 412). https://www.ecb.europa.eu/home/pdf/research/Working_Paper_412.pdf

- Quinn, S. (2008). “The evolution of the check as a means of payment” (Econstor PDF). https://www.econstor.eu/bitstream/10419/57670/1/602139635.pdf

- Bordo, M.D. (Econlib). “Gold Standard” (classical gold standard 1880–1914). https://www.econlib.org/library/Enc/GoldStandard.html

- Bie, U. & Pedersen, A.H. (1999). “The Role of Gold in the Monetary System” (Danmarks Nationalbank PDF). https://www.nationalbanken.dk/media/arboaji0/1999-mon3-role-s19.pdf

- Tallman, E.W. & Moen, J.R. (2007). “Clearing House Loan Certificates…” (PDF). https://www2.oberlin.edu/faculty/rmedia/etallman/ClearingHouseLoanCertificates.pdf

- Federal Reserve History. “The Panic of 1907.” https://www.federalreservehistory.org/essays/panic-of-1907

- Federal Reserve History. “Overview: The History of the Federal Reserve” (founded 1913 for stability). https://www.federalreservehistory.org/essays/federal-reserve-history

- St. Louis Fed. “History and Purpose of the Federal Reserve | In Plain English” (1907 panic → Fed Act). https://www.stlouisfed.org/in-plain-english/history-and-purpose-of-the-fed

- Reserve Bank of Australia (2023). “Bagehot and the Lender of Last Resort – 150 Years On.” https://www.rba.gov.au/speeches/2023/sp-ag-2023-12-14.html

- U.S. Congressional Research Service (2020). “Telegraphs, Steamships, and Virtual Currency…” (Western Union money transfer service, 1871). https://www.congress.gov/crs-product/R46486

- Western Union (2011). “Western Union Celebrates 160 Years of Innovation” (press release; money transfer service 1871). https://ir.westernunion.com/news/archived-press-releases/press-release-details/2011/Western-Union-Celebrates-160-Years-of-Innovation/default.aspx