Early Modern Financial Revolution: Bullion Flows, Stock Markets, Public Debt, and Giro Banking (c. 1500–1700)

“Early modern economies scaled by shifting large payments from coin movement to institutional clearing—banks, markets, and public debt.”

Summary of events during the period

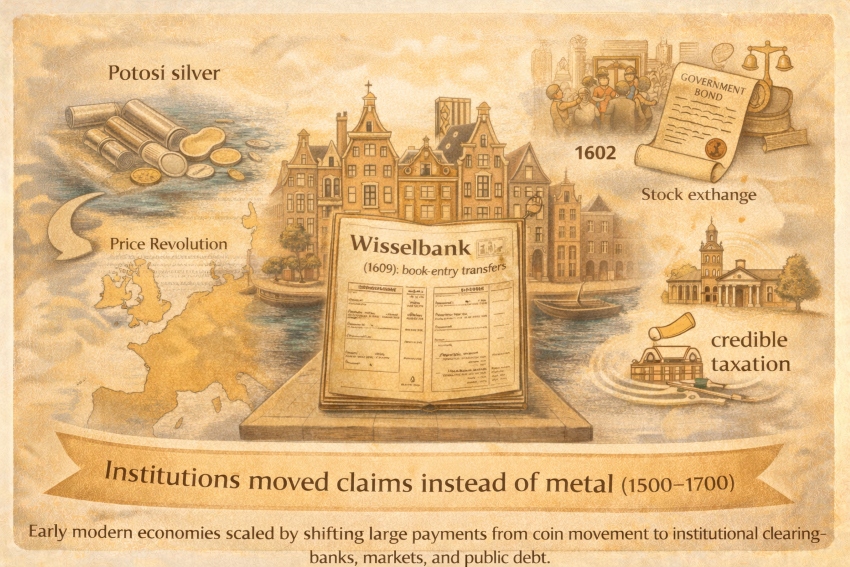

Between 1500 and 1700, European payment systems moved from “coin economies” toward institutionalized finance: public debt instruments, tradable equity, and bank-mediated transfers that reduced the need to ship metal. Two forces interacted. First, vast silver inflows from the Americas (and recurring debasements) contributed to a long inflationary episode often called the Price Revolution, changing how people experienced “prices” and monetary reliability.

Second, commercial states—especially in the Dutch Republic and later England—built durable rails: stock exchanges (VOC shares), municipal giro banks (Bank of Amsterdam), and funded public debt that could be bought and sold. These systems did not eliminate coins; they made coins less central to large-value settlement by moving claims and balances through institutions.

Payment media (what people used to pay)

- Multi-coin circulation + bullion: Early modern Europe still ran on coins, but with persistent problems: many coin types, variable quality, clipping, debasement, and exchange-rate confusion. Giro banking emerges precisely in this environment.

- Book-entry “bank money” (giro balances): The Bank of Amsterdam (Wisselbank), founded in 1609, operated as a municipal payments/giro bank, enabling merchants to settle via transfers between accounts instead of repeated physical coin handling.

- Tradable equity (joint-stock shares): The VOC (1602) issued shares that could be bought and sold; share trading became a durable financing mechanism tied to the Amsterdam securities market.

- Funded public debt (transferable claims on the state): Governments increasingly financed themselves by issuing debt instruments that could be held and traded—expanding the “safe asset” layer that anchored financial systems. England’s late-17th-century shift is a canonical case.

- Early central banking and note experiments (late 1600s): Sweden founded Sveriges Riksbank (1668) after the Stockholms Banco crisis—an early step toward central banking institutions designed to stabilize payments and credit.

How prices were set (negotiated vs administered vs regulated)

Negotiated prices (markets, increasingly integrated)

- Most commodity and wage prices remained negotiated locally, but growing trade networks (and more standardized financial instruments) increased comparability and responsiveness across regions.

Administered/structural drivers (inflationary environment)

- The Price Revolution reflects an environment where monetary conditions (including bullion inflows and debasements) affected the general price level over decades—shaping what “a fair price” looked like in practice even if no authority posted prices.

Regulated standards (money quality and settlement rules)

- Authorities shaped pricing by controlling coin standards, permitting/forbidding certain coin uses, and—critically—by creating institutions (like the Wisselbank) that enforced settlement rules and quality standards for large payments.

How payments cleared (the “rails”)

- Giro clearing (Amsterdam as the model): The Wisselbank cleared debts through book-entry transfers—a large reduction in transaction friction when many coin types circulated. Modern central-bank research characterizes it explicitly as a public giro/payments bank created amid coin debasement and coin heterogeneity.

- Securities-market clearing (shares and debt): Tradable shares and public debt created a new clearing layer: instead of settling every enterprise via one-off merchant loans, firms and states could tap broad investor pools through standardized, transferable claims. The VOC share system and the Amsterdam securities market are the iconic early case.

- Government finance rails (England, 1690s): Parliamentary credibility and dedicated taxation capacity supported government borrowing at scale; the Bank of England (1694) institutionalized government finance and payments in a manner closely associated with England’s “financial revolution.”

- Creditor-protection institutions (Italy as a precedent still relevant): Genoa’s Casa di San Giorgio is widely analyzed as a creditor-protection and public-debt administration institution, illustrating how institutional design can lower repudiation risk and sustain public borrowing.

Trust and governance (why anyone accepted it)

- Rule-based settlement in banks: The Wisselbank’s value proposition was credibility: a supervised settlement venue that reduced disputes over coin quality and enabled reliable large-value payment.

- Constitutional/fiscal credibility for public debt: England’s post-1688 settlement strengthened investor confidence in repayment through taxation under parliamentary control—an explicit emphasis in Parliamentary history material.

- Institutional protection of creditors (public debt as governance): Genoa’s San Giorgio is studied as an arrangement that protected creditors and reduced repudiation risk—turning “state promises” into more durable financial assets.

Revenue model (who made money from the system)

- Banks and correspondents: earned fees/spreads from exchange, settlement, and balance transfers (and, where allowed, from liquidity services). The Wisselbank case is often treated as a payments-bank model with strong implications for fees and public revenue.

- Joint-stock enterprises: financed expansion by selling equity; investors earned returns through dividends and/or secondary-market appreciation (VOC share trading).

- States: expanded fiscal capacity via funded debt—trading future tax revenue for immediate war finance and infrastructure spending; this is central to the late-17th-century English model.

Failure modes and constraints

- Inflation and monetary disorder: prolonged inflationary environments (and coin debasements) increase price volatility and settlement disputes, pushing merchants toward institutional rails where value is better defined.

- Trust collapse in “bank money”: modern central-bank research on the Wisselbank highlights that even sophisticated giro systems can fail if governance weakens and losses become politically or financially untenable.

- Sovereign risk: public debt markets require credible commitment; without strong repayment institutions, borrowing costs rise or markets seize up—precisely why creditor-protection arrangements mattered.

What scaled it (the scaling technology)

- Book-entry settlement (giro banking): transfers between accounts allow netting and reduce transport/security costs—an early “payments network” logic.

- Standardized transferable claims: equity shares and funded government bonds convert projects and wars into investor-readable instruments—scaling capital formation.

- Credible fiscal institutions: dedicated taxation capacity and credible repayment procedures lower borrowing costs and stabilize financial rails.

Caption:

“Early modern economies scaled by shifting large payments from coin movement to institutional clearing—banks, markets, and public debt.”

Sources

- Bank for International Settlements (BIS), Bolt (2023), “The Bank of Amsterdam and the limits of fiat money” (working paper, PDF). :contentReference[oaicite:25]{index=25}

- Federal Reserve Bank of Atlanta, Quinn & Roberds (2006), “An Economic Explanation of the Early Bank of Amsterdam…” (PDF). :contentReference[oaicite:26]{index=26}

- De Nederlandsche Bank (DNB), Frost et al. (2020), “An early stablecoin? The Bank of Amsterdam…” (PDF). :contentReference[oaicite:27]{index=27}

- WA Museum, “VOC – United Dutch East India Company” (shares, share trading). :contentReference[oaicite:28]{index=28}

- Beursgeschiedenis.nl, “The Story” (VOC 1602; Amsterdam Stock Exchange origin narrative). :contentReference[oaicite:29]{index=29}

- UK Parliament, “The Financial Revolution” (Bank of England 1694; parliamentary taxation credibility). :contentReference[oaicite:30]{index=30}

- Bank of England, “History” (founded 1694 as banker to government). :contentReference[oaicite:31]{index=31}

- Encyclopaedia Britannica, “History of Europe: Prices and inflation” (Price Revolution context; debasements). :contentReference[oaicite:32]{index=32}

- Brill (book chapter PDF), “Potosí in the Global Silver Age” (silver production and monetary effects context). :contentReference[oaicite:33]{index=33}

- Fratianni (PDF), “Government Debt, Reputation and Creditors’ Protections” (Casa di San Giorgio as creditor-protection institution). :contentReference[oaicite:34]{index=34}

- Sveriges Riksbank, “Sveriges Riksbank is founded” (1668; oldest central bank). :contentReference[oaicite:35]{index=35}