Medieval Europe: Fairs, Bills of Exchange, and “Invisible” Payments (c. 1100–1500)

“Medieval European finance: a trade fair with money-changers and mixed coins, a bill of exchange moving value between cities, and merchant-law enforcement enabling long-distance settlement (1100–1500).”

Summary of events during the period

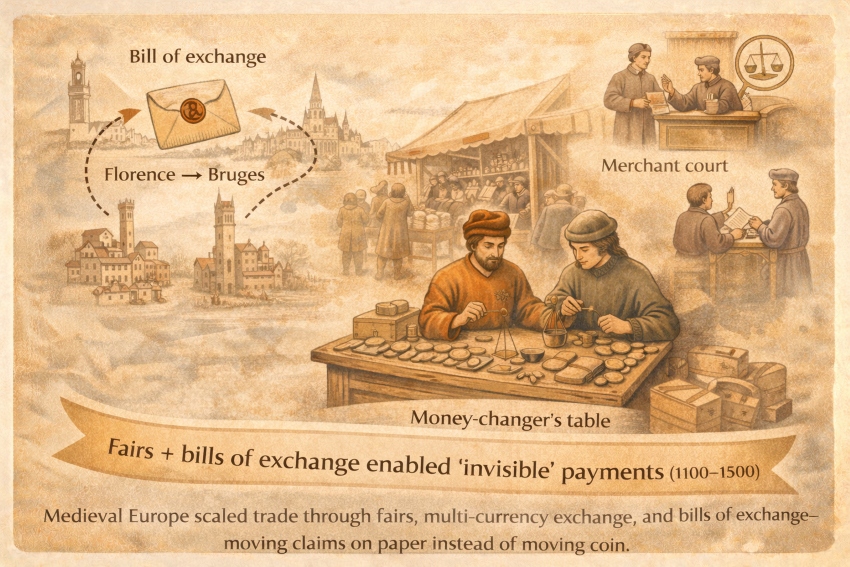

From roughly 1100 to 1500, European commerce scaled through a distinctive combination of trade fairs, multi-currency exchange, and written credit instruments that reduced the need to move coin physically. The Champagne fairs (12th–13th centuries) are a canonical example of how institutions, enforcement, and finance co-evolved to support long-distance trade. Over time, merchants increasingly settled through bills of exchange/letters of exchange, correspondent networks, and merchant-law enforcement—creating “invisible” payments (claims moving on paper) layered on top of a still very real world of coins, weights, and money-changers.

Payment media (what people used to pay)

- Coins (high diversity, local and foreign): Medieval Europe was a multi-mint environment. Merchants routinely handled different coin types and needed exchange services and quality verification (weight/fineness).

- Money-changing + bullion-by-weight as a bridge: Where coin quality differed, professional changers and weight standards helped price and settle across currencies (a practical continuation of “money-by-weight” logic inside a coin world).

- Bills of exchange (letters of exchange): A bill of exchange became a major tool for settling international trade, allowing merchants to avoid shipping bullion/coin and instead move paper claims through networks of correspondents—becoming widely used in the 13th century among Lombards/Italian merchants.

- Fair settlement instructions (“letters of fair”) and netting: At exchange fairs, written instructions and standardized procedures enabled settlement of multiple obligations—often by offsetting claims rather than paying everything in coin.

How prices were set (negotiated vs administered vs regulated)

Negotiated prices (core market mechanism)

- Most commercial pricing remained negotiated, especially for merchant goods traded at fairs and in urban markets. The innovation was not “fixed prices,” but lower transaction friction (clearer units, more reliable settlement, enforceable contracts).

Administered components (tolls, seigneurial rights, and market access)

- Authorities shaped the cost structure through tolls, fees, privileges, and protections surrounding fairs and trade routes. In practice, these charges influenced final prices even when the state did not dictate the market price.

Regulation through standards and merchant law

- A major regulatory layer was institutional: merchant courts and law-merchant norms enforced commercial expectations quickly in trading corridors, which is crucial when parties are foreign and disputes must be resolved on time-sensitive schedules.

How payments cleared (the “rails”)

- Bills of exchange as an international settlement rail: The bill of exchange is widely described as the most important written instrument in the late medieval international financial world. It cleared payments by moving a claim payable in another place/currency through correspondent relationships.

- Fair-based clearing and netting: Exchange fairs supported periodic settlement cycles—merchants could net multiple obligations, reducing the need for physical coin transfers and lowering security risk.

- Faster dispute resolution via merchant law mechanisms: A merchant-law environment (lex mercatoria / “law merchant”) is commonly characterized as a body of translocal commercial norms enforced through merchant courts and practices along trade routes—helping contracts function when state courts were slow or fragmented.

- Accounting as operational infrastructure: As transaction volume increased, bookkeeping systems improved. Scholarship on double-entry accounting places its emergence in medieval Italy (13th century) and its spread thereafter as a scalable method for controlling complex commercial operations.

Trust and governance (why anyone accepted it)

- Institutional trust at fairs: Research on the Champagne fairs emphasizes that success relied on enforceable institutions supporting impersonal exchange—credibility and enforcement mattered as much as geography and goods.

- Merchant-law enforcement: Lex mercatoria is described in authoritative legal reference works as relatively autonomous, merchant-generated commercial norms that supported cross-border trade where a single state legal system could not.

- Network trust (correspondents + reputation): Bills of exchange required dependable correspondents in different cities; the “trust layer” is relational and institutional, reinforced by repeat dealings and enforceable protest/collection practices.

Revenue model (who made money from the system)

- Foreign exchange spreads and commissions: Bills of exchange embed fees and FX spreads as a business model for merchant-bankers and correspondents. This becomes a durable revenue engine because trade requires currency conversion and time-delayed settlement.

- Intermediation rents (brokers, money-changers, notaries): Specialists earned fees by verifying coin quality, arranging deals, recording contracts, and enforcing claims.

- Rulers and towns (tolls, privileges, and market rights): Hosting fairs and controlling trade corridors created revenue through tolls and the sale of protections/privileges—an institutional business model layered on commerce.

Failure modes and constraints

- Default and fraud risk: A paper-claims system concentrates counterparty risk; enforcement mechanisms (merchant courts, protests, reputational sanctions) exist because failures were common enough to matter.

- Currency risk and debasement: Multi-mint coinage creates persistent valuation and quality problems, increasing transaction costs and motivating “paper rails” to reduce repeated handling of coin.

- Political and war shocks: Route insecurity, confiscation, and shifting sovereign control can break correspondent networks and fair cycles.

What scaled it (the scaling technology)

- Bills of exchange (paper rails): reduced transport risk and enabled cross-border settlement through correspondent networks.

- Periodic settlement hubs (fairs): concentrated trade, information, and enforcement into predictable cycles—helping merchants coordinate and clear obligations.

- Accounting discipline (double-entry emergence): improved internal control and multi-transaction visibility, enabling firms to scale beyond what memory or single-entry accounts could reliably manage.

Caption:

“Medieval Europe scaled trade through fairs, multi-currency exchange, and bills of exchange—moving claims on paper instead of moving coin.”

Sources

- Edwards, J. & Ogilvie, S. (2012). What lessons for economic development can we draw from the Champagne fairs? (Cambridge, PDF).

- Encyclopaedia Britannica. “Bill of exchange” (origins; widespread 13th-century use in Northern Italy; settlement in international trade).

- Bolton, J. (2021). “‘Your flexible friend’: the bill of exchange…” Economic History Review (importance in late medieval international finance).

- Oxford Reference. “Bills of Exchange” (remittance + credit; correspondent network dependence).

- Oxford Public International Law (EPIL). “Lex mercatoria” (law-merchant characteristics and autonomy).

- OpenEdition Books. I. The Exchange Fairs: a Brief History (letters of fair; settlement procedures).

- The Accounting Review (2016). “The Genesis of Double-Entry Bookkeeping” (emergence in 13th-century Italy).