Classical Financial Infrastructure: Banking, Credit, and Public Finance (c. 300 BCE–200 CE)

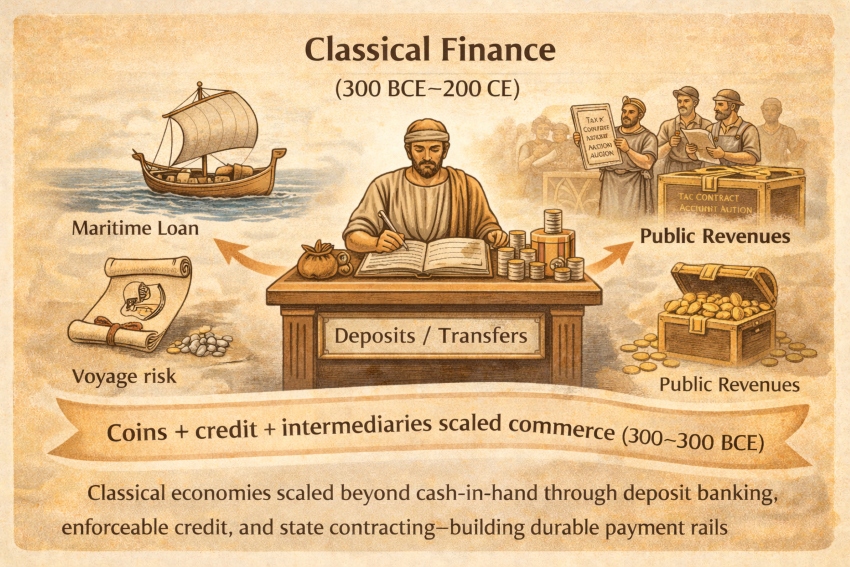

“Classical economies scaled beyond cash-in-hand through deposit banking, enforceable credit, and state contracting—building durable payment rails for trade and public finance.”

Summary of events during the period

Between roughly 300 BCE and 200 CE, the Mediterranean economy developed financial “infrastructure” that went beyond coins in circulation. Markets still relied heavily on cash, but a growing share of higher-value commerce and public finance ran through credit contracts, deposit banking, account transfers, and state contracting. The clearest evidence comes from (1) Greek commercial lending, especially maritime loans; (2) Hellenistic state finance, especially in Ptolemaic Egypt with royal banks and transfer accounting; and (3) Roman financial intermediation, including deposit bankers (argentarii) and large-scale public contracting (publicani).

Payment media (what people used to pay)

- Coins as the everyday settlement layer: Coinage is ubiquitous, but its most important role in this epoch is as the standardized “cash leg” that supports contracts, taxes, and accounting at scale.

- Bank deposits and account transfers (cashless settlement): Greek and Roman banking practice increasingly included deposit-taking and transfers, allowing parties to settle transactions without physically moving large amounts of coin every time. Greek bankers’ functions included receiving deposits, lending, and testing coin; Roman evidence describes argentarii operating in deposit-banking-like ways.

- Commercial credit instruments: Maritime loan contracts financed overseas trade (high risk, high return), structured around the voyage and enforceable through courts. A well-known 4th-century BCE example is a loan financing an Athens–Black Sea voyage and return (a template for how trade credit worked).

- State receipts and fiscal settlement (especially in Egypt): In Ptolemaic and early Roman Egypt, papyri preserve a dense documentary environment (receipts, accounts, tax records) linked to state finance and banking operations.

How prices were set (negotiated vs administered vs regulated)

Negotiated prices (most market exchange)

- For ordinary goods in marketplaces, prices are best modeled as negotiated and locally determined, with coin denominations making price quotation easier but not eliminating bargaining.

Administered prices and terms (state procurement, taxation, and institutional supply)

- Large institutions shaped “effective prices” via procurement, taxation-in-kind vs cash assessment, and official settlement channels—especially visible in the papyrological record of Egypt’s fiscal administration.

Regulation as market-shaping (standards, courts, and enforcement)

- Rather than setting all prices, states often influenced exchange by enforcing weights/coin standards, defining legal remedies, and policing fraud—lowering transaction costs and increasing market participation.

How payments cleared (the “rails”)

- Bank-mediated transfers (Greek and Roman): Banking could clear payments through book transfers—debiting one party’s deposit and crediting another—reducing the physical handling and transport risk of coin. Greek banking roles include document custody and coin testing; Roman scholarship emphasizes deposit-banking-like functions and a broader money supply impact via intermediation.

- State banking and giro-like mechanisms (Ptolemaic Egypt): Research on Ptolemaic royal banks describes transfer accounting systems tied to fiscal administration, indicating a more centralized “payments + tax” infrastructure than in most city-state contexts.

- Court-enforced commercial credit (Athenian maritime loans): Disputes over maritime loans appear in Attic oratory and later scholarship precisely because these contracts were formal, high-stakes, and litigated—a sign of mature commercial enforcement.

Trust and governance (why anyone accepted it)

- Legal enforceability: The credibility of credit depended on courts, documentation, witnesses, and reputational networks. Maritime loans are especially revealing because lenders relied on contracts and litigation when voyages went wrong.

- Banker credibility and procedures: Bankers’ roles as coin testers, document keepers, and settlement intermediaries are trust technologies: they reduce counterparty risk and informational friction.

- State credibility and administrative capacity (Egypt): Where banking is fused with fiscal administration, trust is partly institutional—anchored in state recordkeeping and collection systems.

Revenue model (who made money from the system)

- Interest and risk pricing: Credit generates revenue through interest; maritime lending prices risk explicitly (voyage risk, seasonality, ship loss, enforcement cost).

- Banking spreads and fees: Deposit banking and payment services create income through spreads (borrow vs lend), fees, and privileged access to liquidity and information.

- Public contracting and tax farming (Rome): Public revenues could be contracted out; the publicani concluded contracts for public revenues and related services—creating a scalable revenue model where private actors profit from state finance operations.

Failure modes and constraints

- Maritime credit risk: Shipwreck, seizure, delay, and dispute are inherent—hence the heavy legal footprint of maritime loans.

- Liquidity stress and political shock: War, confiscation, abrupt policy shifts, and localized shortages can break settlement chains even with sophisticated institutions.

- Agency and corruption risk (state contracting): Tax farming and public contracting introduce principal–agent problems and incentives to overextract—an enduring tension in outsourced revenue collection.

What scaled it (the scaling technology)

- Standardized coin systems + denominations: the universal cash layer that makes contracts and prices legible.

- Durable documentation at volume: papyri, tablets, receipts, and account books make claims transferable and auditable—especially visible in Egyptian archives.

- Intermediation (banks and contractors): deposit banks and public contractors scale finance by pooling, netting, and enforcing payments beyond what direct barter or isolated cash exchange can efficiently support.

Caption:

“Classical economies scaled beyond cash-in-hand through deposit banking, enforceable credit, and state contracting—building durable payment rails for trade and public finance.”

Sources

- Millett, P. “Credit Where It’s Due…” (Greek bankers’ functions: deposits, lending, testing coin, document custody).

- “Athenian Finance: Maritime and Landed Yields” (JSTOR; maritime finance evidence).

- “Athenian Finance” (chapter noting a detailed maritime loan contract financing a voyage).

- Oxford Academic chapter: “Credit and Financial Intermediation” (argentarii as deposit bankers; intermediation expands money supply).

- Temin, P. “Financial intermediation in the early Roman Empire” (MIT working paper; deposits/loans/intermediation).

- Oxford Bibliographies: “Banking in the Roman World” (scholarly overview and evidence base).

- Brill Reference Works: “Publicani” (public revenue contracts and contractors).

- Gutiérrez (2022). “Tax collection in the Roman Empire…” (institutional analysis of tax farming and evolution).

- Muhs (2018). “Institutional models for Ptolemaic royal banks…” (transfer accounting in royal banking).

- Cambridge Core (chapter PDF): “Cash and credit” (Egyptian basilike trapeza and fiscal-banking linkage).